is well-positioned for business growth")

Just because a company isn’t making profits doesn’t mean its stock price will go down. For example, Amazon.com lost money for years after going public, but if you had bought and held the stock since 1999, you could have made a lot of money. But the harsh reality is that too many loss-making businesses run out of cash and go bankrupt.

So the obvious question is, Yassen Holding (NYSE:YSG) shareholders are debating whether they should be worried about the company’s cash burn rate. In this article, we define cash burn as the amount of cash a company spends each year to fund growth (also known as negative free cash flow). First, we compare its cash burn to its cash reserves to calculate its cash runway.

Check out our latest analysis for Yassen Holding.

Does Yassen Holding have long-term financing potential?

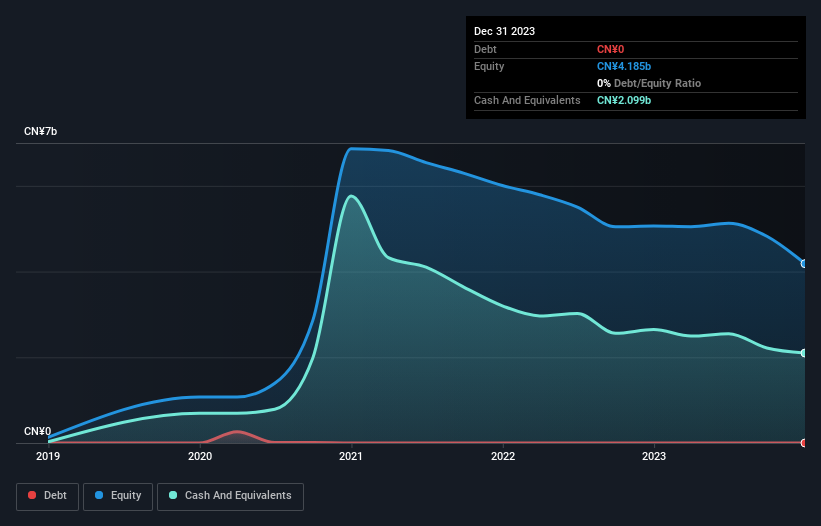

A company’s cash runway can be calculated by dividing the amount of cash it holds by the rate at which it spends that cash. As of December 2023, Yassen Holding had cash of CA$2.1 billion and no debt. Last year’s cash burn was CA$151m. This means that the company had a very long cash runway as of December 2023. Notably, however, analysts believe Yassen Holding will reach breakeven (at a free cash flow level) by then. In that case, you may never reach the end of your financial runway. You can see how its cash holdings have changed over time, as shown below.

Is Yatsen Holding’s revenue increasing?

Yassen Holding actually had positive free cash flow last year, so we’d be hesitant to extrapolate from recent trends to assess its cash burn. So measuring operating revenue growth is probably the best bet at this point. Unfortunately, last year saw disappointing results, with operating revenue for the same period falling 7.9%. However, it is clear that the key factor is whether the company will grow its business going forward. For this reason, it makes a lot of sense to see what analysts are predicting for the company.

How easily can Yassen Holding raise funds?

Given Yassen Holding’s declining earnings, Yassen Holding shareholders will need to consider how the company can fund growth if it proves to need more cash. . Generally, listed companies can raise new cash by issuing stock or taking on debt. Many companies end up issuing new shares to fund future growth. You can compare a company’s cash burn to its market capitalization to find out how many new shares a company needs to issue to finance its operations for one year.

Yatsen Holding has a market capitalization of CA$3.4 billion and burned through CA$151 million last year, representing 4.5% of its market value. Given that this is a fairly small percentage, it would probably be very easy for the company to fund another year of growth by issuing new shares to investors or taking out a loan.

How risky is Yassen Holding’s cash burn situation?

As you’ve probably already noticed, we’re relatively happy with how Yassen Holding is burning through cash. In particular, we think the company’s ability to raise funds stands out as evidence that the company is spending well. Although the decline in revenue was not large, the other factors mentioned in this article more than compensate for this metric’s weaknesses. It’s clearly very positive that the analysts are predicting that the company will reach breakeven soon. Considering all the factors in this report, we think the business has plenty of capital to spend if needed, so we’re not worried about cash burn at all.A detailed investigation of the risks revealed 1 warning sign for Yatsen Holding Here’s what readers should consider before investing money in this stock.

of course Yassen Holding may not be the best stock to buy.So you might want to see this free A collection of companies with a high return on equity, or a list of stocks that insiders are buying.

Have feedback on this article? Curious about its content? contact Please contact us directly. Alternatively, email our editorial team at Simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary using only unbiased methodologies, based on historical data and analyst forecasts, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.