is 125.00 yen")

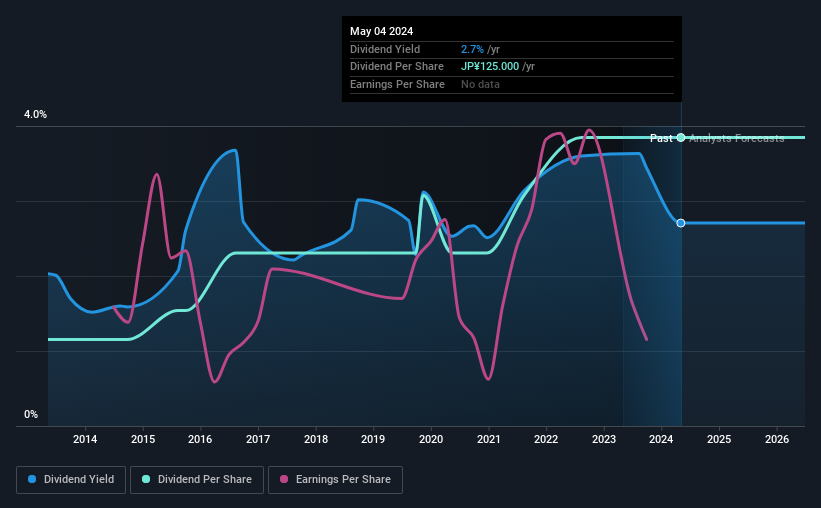

board of directors of Integrated Design & Engineering Holdings Co., Ltd. TSE 9161 announced that it will pay a dividend of 125 yen per share on September 12th. Based on this payment, the dividend yield is 2.7%, which is fairly typical for the industry.

Check out our latest analysis for Integrated Design & Engineering HoldingsLtd.

Integrated Design & Engineering HoldingsLtd’s earnings easily cover distributions

I’m not very impressed with the dividend yield unless it can be maintained over the long term. The last payment accounted for 87% of the revenue, but the cash flow was much higher. Since dividends only pay out cash to shareholders, we focus on the cash payout ratio, which shows that there is enough money left over to reinvest in the business.

Looking ahead, we expect earnings per share to increase dramatically over the next year. If recent dividend patterns continue, the payout ratio could reach a fairly sustainable 26%.

Dividend volatility

The company’s dividend history has been characterized by instability, with the dividend cut at least once in the past 10 years. Since 2014, his annual payment at that time was 37.50 yen, but his recent annual payment was 125.00 yen. This means that the company grew its distribution at approximately 13% per year over that period. Integrated Design & Engineering HoldingsLtd has been growing its dividend rapidly, despite cutting it at least once in the past. I would be wary of buying this stock solely for the dividend income, as companies that have cut back often tend to cut back again.

Dividend growth is questionable

With a relatively unstable dividend, it is even more important to assess whether earnings per share are growing, which could indicate future dividend increases. Over the past five years, Integrated Design & Engineering Holdings Ltd’s earnings per share have decreased by approximately 7.5% annually. If a company’s earnings decline over time, it stands to reason that its dividend payments must also be reduced. However, it’s not all bad news. Revenues are expected to increase over the next 12 months. Until this becomes a long-term trend, we’ll be a little cautious.

Integrated Design & Engineering Holdings Co., Ltd.’s philosophy regarding dividends

In summary, while it’s good to see that the dividend hasn’t been cut, we’re a bit cautious about Integrated Design & Engineering HoldingsLtd’s payments, as there may be some issues with sustaining them in the future. . Payouts have been erratic so far, but the dividend could become reliable in the short term if the company generates enough cash to cover it. You’ll probably look elsewhere for more profitable investments.

It’s important to note that companies with a consistent dividend policy generate greater investor confidence than companies with an erratic dividend policy. At the same time, there are other factors that readers should be aware of before pouring capital into stocks. For example, we identified 2 warning signs for Integrated Design & Engineering HoldingsLtd What you need to know before investing.Looking for more high-yield dividend ideas? Try ours A group of people with strong dividends.

Valuation is complex, but we help make it simple.

Please check it out Integrated Design Engineering Holdings Co., Ltd. Could be overvalued or undervalued, check out our comprehensive analysis. Fair value estimates, risks and caveats, dividends, insider trading, and financial health.

See free analysis

Have feedback on this article? Curious about its content? contact Please contact us directly. Alternatively, email our editorial team at Simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary using only unbiased methodologies, based on historical data and analyst forecasts, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.